BNEF’s new energy report highlights scenarios to reach climate neutrality by 2050

Achieving net-zero carbon emissions by 2050 will require as much as US$173 trillion in investments in the energy transition, according to BloombergNEF’s (BNEF) New Energy Outlook 2021 (NEO). The report outlines three distinct scenarios (labelled Green, Red and Gray) that each achieve net-zero while relying on a different mix of technologies.

According to BNEF, the energy transition requires very substantial investments in infrastructure, with capital flowing away from fossil fuels and toward clean power and other climate solutions. Despite uncertainty around the overall cost of each NEO scenario set out, BNEF estimates investment in energy supply and infrastructure amounts to between US$92 trillion and US$173 trillion over the next thirty years. Annual investment will need to more than double to achieve this, rising from around US$1.7 trillion/ year today, to somewhere between US$3.1 trillion and U$5.8 trillion/year on average over the next three decades.

“The capital expenditures needed to achieve net zero will create enormous opportunities for investors, financial institutions and the private sector, while creating many new jobs in the green economy,” said Jon Moore, CEO of BNEF.

BNEF stated that renewable energy and electrification are the backbone of the transition and must be accelerated immediately, while hydrogen, carbon capture and new modular nuclear plants are emerging tools that should be developed and deployed as soon as possible. The next nine years will be crucial to getting on track to limit rising temperatures in line with the Paris Climate Agreement, and require a rapid doubling of current annual investment of US$1.7 trillion in the energy system.

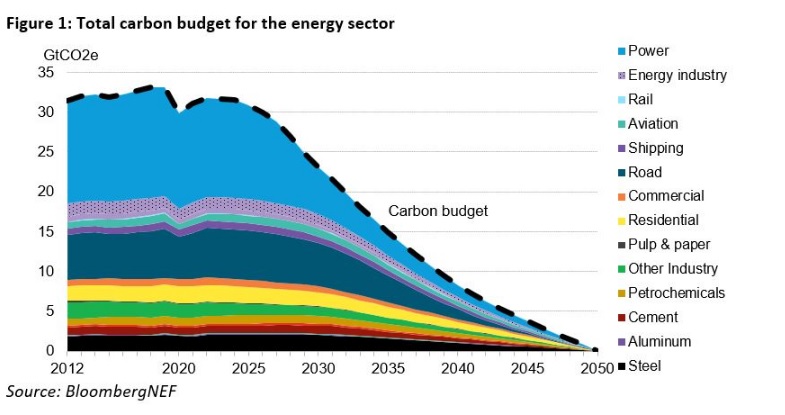

A core part of the BNEF analysis is constructing sector by sector emissions budgets to achieve net-zero in 2050 with an orderly transition. Together, these show that global energy-related emissions need to drop 30% below 2019 levels by 2030, and 75% by 2040, to reach net-zero in 2050. This is a 1.75 degree equivalent budget that implies a 3.2% reduction each year to 2030 and a swift reversal of recent trends: emissions rose 0.9% a year from 2015 to 2020.

The power sector needs to make the greatest progress over the next decade, reducing emissions by 57% from 2019 levels by 2030, and then 89% by 2040. Yet every sector of the energy economy needs to cut emissions steeply to achieve net-zero. Road transport emissions must fall 11% by 2030, then drop faster during the 2030s to reach 80% below 2019 levels in 2040. In order to achieve these drastic emissions reductions in line with a long-term trajectory to net-zero this decade commercially available abatement technologies need to be deployed in each sector.

More than three quarters of the effort to cut emissions in the next nine years falls to the power sector and to faster deployment of wind and solar PV. Another 14% is achieved with greater use of electricity in transport, in heating for buildings and in providing low-temperature heat in industry. Greater recycling in steel, aluminum and plastics accounts for a 2% drop in emissions, greater building efficiency 0.5%, and growth of bioenergy for sustainable aviation fuel and shipping another 2%. This period also requires the piloting and scaling-up of new technology for deep decarbonisation post 2030.

“There is no time to waste. If the world is to achieve or get close to meeting net zero by mid-century, then we need to accelerate deployment of the low-carbon solutions we have this decade – that means even more wind, solar, batteries, and electric vehicles, as well as heat pumps for buildings, recycling and greater electricity use in industry, and redirecting biofuels to shipping and aviation,” said BNEF chief economist Seb Henbest.

Specifically, the following milestones will need to be achieved by 2030 to be on track to reach net-zero by mid-century, including adding 505 GW of new wind power each year to 2030 (5.2 times the 2020 total); GW of solar PV each year to 2030 (3.2 times the 2020 total); 245 GWh of batteries each year to 2030 (26 times the 2020 total); and 35 million EVs added to the road each year to 2030 (11 times the 2020 total), as well as to make sustainable aviation fuels make up 18% of aircraft fuel in 2030 .

Also, there should be increased recycled volume of aluminum by 67%, steel by 44% and plastics by 149% by 2030 from 2019 levels; deployment of 18 million heat pumps each year to 2030; increase electricity use to lower temperature heat in industry 71% from 2019 levels by 2030 ; and reduction of coal-fired power generation by 72% from 2019 levels by 2030, and retirement of up to 70%, or 1,417 GW, of coal-fired power capacity by 2030

Some 83% of primary energy is currently fossil fuels, while wind and solar PV account for 1.3%. In BNEF’s Green Scenario, which prioritises clean electricity and green hydrogen, wind and solar grow to 15% of primary energy in 2030, and 70% in 2050. In contrast, fossil fuels drop some 7% a year, and account for just 10% of supply by 2050. In the Red Scenario, which prioritises nuclear for hydrogen production, nuclear fuel makes up a whopping 66% of primary energy in 2050, compared with 5% now. In contrast, BNEF’s Gray Scenario, where widespread use of carbon capture and storage means coal and gas continue to be used, fossil fuels decline just 2% a year, to 52% of primary energy supply in 2050, with wind and PV growing to 26%.

Electrification plays a large role. Across all scenarios, the use of electricity in industry, transport and buildings raises its share of total final energy to just below 50% in 2050, from 19% today. As a result, electricity generation is almost 62,200 TWh by 2050 in BNEF’s Gray Scenario – more than double the 2019 total. But in the Green Scenario, where electricity is also used to produce large quantities of hydrogen, power generation is twice as large again – more than 121,500 terawatt-hours, or roughly 4.5-times 2019 levels. This is split between green hydrogen production, which takes 49%, and 51% that is consumed directly in the end-use economy.

Emissions reductions in the power sector are driven predominantly by new wind and solar, which provide between 59% and 65% of the cuts in BNEF’s scenarios. This requires a big step up. While the first 1,000 GW of wind and PV took twenty years to deploy, getting to zero emissions in the Green Scenario requires around 1,400 GW of renewables to be deployed every year, on average, for the next three decades. In our Green Scenario the market opportunity for renewables is staggering:

Wind: 25 TWs in 2050, or average of 816 GW/year installed to 2050

Solar: 20 TW in 2050, or average of 632 GW/year installed to 2050

Batteries: 7.7 TWh in 2050, or average of 257 GWh/year installed

Variable renewables account for 54% of electricity generation in 2030, then 78% in 2040, and 84% in 2050.

“The energy transition is inherently uncertain,” said Matthias Kimmel, BNEF’s head of energy economics. “This is why we have modelled three distinct pathways to net zero this year. Hydrogen, nuclear and carbon capture could all play an important role in helping the world reach net-zero, and each of these technologies must be further developed and brought to market in the coming decade, if they are to realise their potential.”

Hydrogen must scale rapidly from its current very small base, but the size of its role varies widely by scenario. New demand for hydrogen in 2050 is just 190 MMT in BNEF’s Gray Scenario, compared with 1,318 million tonnes in the Green Scenario, where it increases to around 22% of total final energy consumption, compared with less than 0.002% today. Hydrogen has many applications as an energy carrier and for emissions abatement to help meet the net-zero target in each scenario, whether displacing fossil-fuel combustion in industry, buildings and transport or complementing renewables to help meet seasonal demand in the power sector.

Carbon capture and storage technologies, or CCS, can be applied across a variety of processes that emit carbon dioxide, including power generation and aluminum, steel and cement production. Widespread use of CCS captures over 174 gigatonnes of carbon dioxide over the outlook to 2050, in BNEF’s Gray Scenario. In this scenario, in which coal and gas can continue to be used, fossil fuel demand declines 2% a year, but still makes up 52% of primary energy in 2050.

In BNEF’s Red Scenario, which prioritises nuclear power, there are 7,080 GW of nuclear capacity by 2050. This is about 19-times the nuclear power capacity installed globally today. Just under half of this is used to generate electricity in the end-use economy, where smaller, more modular reactors complement renewables. The rest is made up of dedicated nuclear plants that power electrolysers producing so-called ‘red hydrogen’. This nuclear renaissance drives uptake of nuclear fuel, which eventually dominates primary energy supply, making up 44% in 2040 and two thirds in 2050.

Demand for fossil fuels sees a significant decline over the next 30 years in all scenarios, according to the BNEF analysis. The Green and Red Scenarios show demand for coal, oil and gas for combustion drop to zero by 2050, replaced by renewables, electricity and hydrogen. Fossil fuels fare better in the Gray Scenario, where CCS offers a way forward for coal in power generation and industry, and reverses some of the decline seen in gas from 2030. However, it does little to support oil, which is predominantly used in transport, where CCS can barely play a role. (Press Release)