Europe stockpiles EUR7 bn Chinese solar panels as imports outpace installations

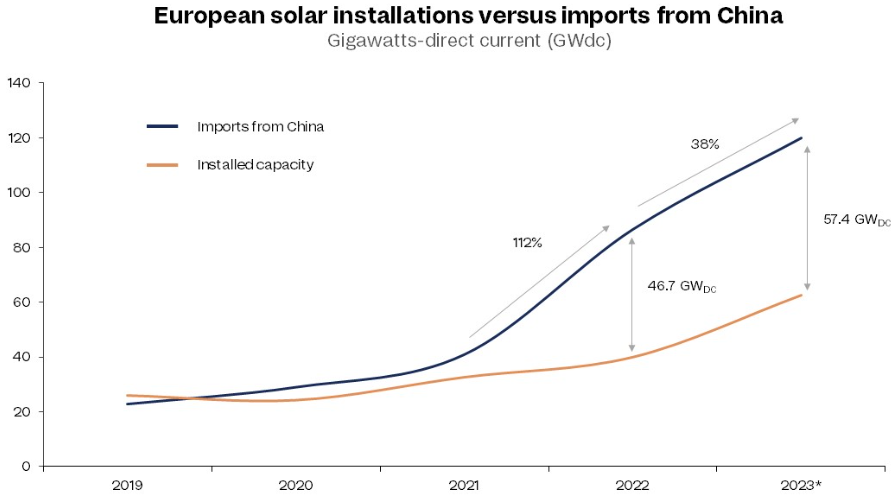

Chinese-manufactured solar photovoltaic (PV) panels are piling up in European warehouses, with approximately 40 gigawatts-direct current* (GWdc) of capacity currently in storage – the same amount installed across the continent in 2022. These solar panels in storage are worth about EUR7 billion and could generate enough electricity to power 20 million homes per year. The build-up is only set to grow this year, with Rystad Energy forecasting 100 GWdc of solar capacity in storage by the end of 2023, according to Rystad Energy, an independent energy research and business intelligence company.

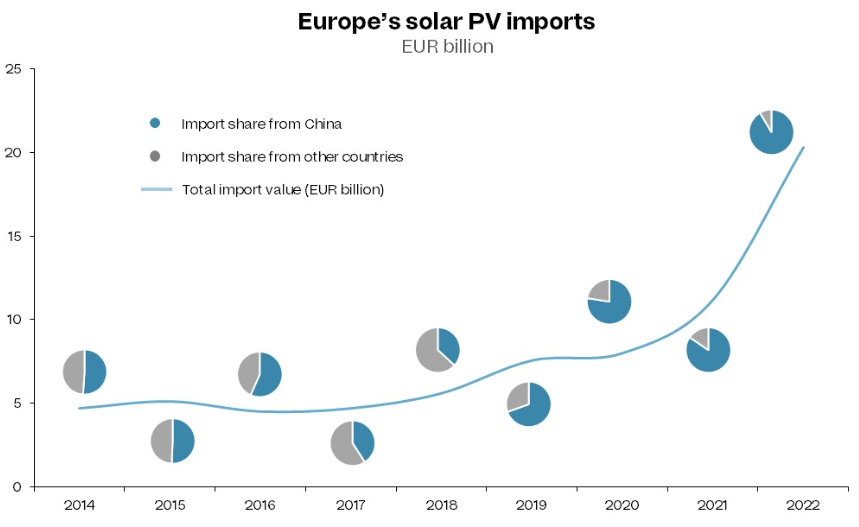

Europe’s spending on solar imports has almost quadrupled in the last five years, surging from EUR5.5 billion in 2018 to more than EUR20 billion last year, while the supply source has become increasingly concentrated. An overwhelming EUR18.5 billion, equal to 91% of all PV import expenditure, was spent on Chinese products, as volatile panel prices impacted buying decisions. A critical shortage of solar-grade polysilicon – a crucial raw material in manufacturing PV modules – in 2021 and 2022, coupled with rising demand for installed solar PV, contributed to soaring panel prices worldwide. As China dominates both the production and processing of polysilicon into PV modules, Chinese manufacturers have been increasingly able to undercut the competition on price. Today, panels made in China often cost as little as two-thirds of European-manufactured capacity.

Market watchers might think that the healthy inventory levels could signal an import slowdown on the horizon, but the first few months of 2023 tell a different story. Imports in January were 17% higher compared to 2022, with February up 22%, March surging 51%, April up 16%, and May growing 6% over last year. If current import levels continue, 2023 will be a record-breaking year for imports and inventory. Annual imports look set to hit 120 GWdc, far surpassing expected capacity installations of 63 GWdc.

“European countries are desperate to get their hands on affordable solar infrastructure to advance their renewable energy targets, decarbonize and avoid paying elevated prices for new capacity. Although efforts are underway to build a reliable solar supply chain in Europe, the need for panels now means leaders cannot wait until 2025 or later to buy European,” says Marius Mordal Bakke, senior supply chain analyst at Rystad Energy.

Energy policies and the green transition continue to drive demand for European solar PV growth. Since 2022, the Green Deal Industrial Plan (GDIP), REPowerEU, and the Net Zero Industry Act have all set ambitious solar PV goals. These goals include a target for 30 GWdc of European manufacturing along the entire value chain by 2025 and 40% of installed solar PV being manufactured within the continent by 2030.

Despite these ambitious goals, between 2019 and 2022, locally-made modules could not keep pace with the growth of imported panels. From 2021 to 2022, the amount of Chinese solar modules imported by European countries increased by 112% to about 87 GWdc. The installation rate in these countries has yet to meet anticipated levels, resulting in a sizeable gap of almost 47 GWdc in 2022 in shipped versus installed modules.

Judging by the market in 2023 to date, we expect Chinese imports to increase by 38% annually and reach 120 GWdc. While installations will gain momentum – jump 57% versus last year to hit about 63 GWdc – the gap will widen in absolute terms, with a difference of 57.4 GWdc at year end.

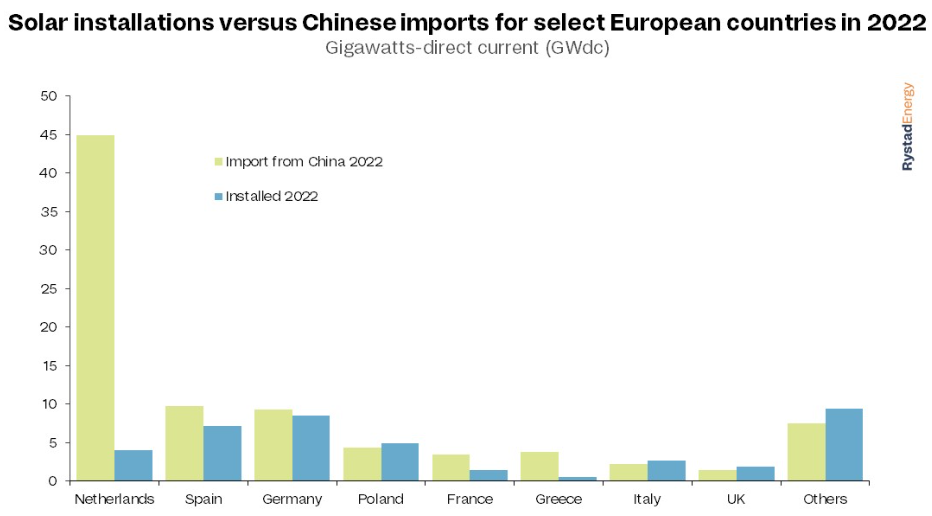

The imports are heading to several key destinations, including the Netherlands, Spain, Germany, Poland, France, Greece, Italy, and the UK. The Netherlands was the standout leader in Chinese PV imports in 2022, bringing in almost 45 GWdc alone, more than ten times the amount of panels installed domestically across the year. Spain, Germany and France also imported more panels from China than they installed from any source. Greece has a similar profile to the Netherlands but on a smaller scale, with the country installing the equivalent of only 15% of the capacity imported from China.

Despite last year’s stockpiling, enduring robust imports and muted solar installation activity will inevitably lead to overstocking in Europe. Solar PV installation bottlenecks – like labor shortages and critical material delays – will most likely sustain until 2025, but the continent’s excessive inventory means panel prices are unlikely to see any meaningful increases.

With the current technology transition in the solar industry – from P-type to N-type cells – and incentives for purchasing European-manufactured panels, stockpiled products could face declining interest from European buyers if left in storage too long. However, that is not likely in the short term until the continent can advance its manufacturing capabilities.