South Korea/Japan face power hikes due to Middle East crisis

Against the back of the Middle East war, Asia spot LNG prices have surged 94% and coal prices have jumped 17-31% since the conflict began, but the impact on global electricity markets is splitting dramatically between winners and losers. A new insight from Wood Mackenzie shows that while countries like Japan, South Korea, and Italy face potential cost increases of up to 80%, while the US and Brazil remain largely insulated from the turmoil.

Wood Mackenzie’s insight, “The Great Power Divide: The Middle East crisis is splitting global power markets into winners and losers “, analyses how 13 representative power markets are being impacted by the ongoing crisis, with exposure determined primarily by generation mix and fuel import dependency.

“While some markets face significant cost escalation and potential supply constraints, others remain largely insulated from international fuel market volatility due to their reliance on strong domestic thermal supplies or a large network of renewable energy,” said Peter Obaldstone, Research Director, Europe Power for Wood Mackenzie.

Vulnerability – most exposed to least exposed

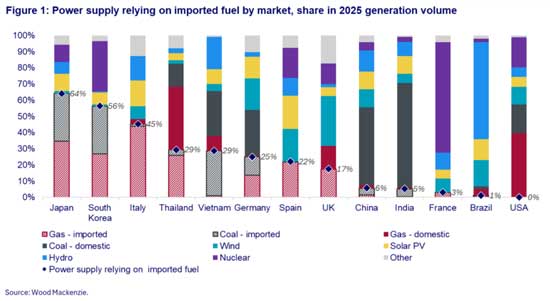

In the study, Wood Mackenzie finds that Japan represents the most exposed major power market globally, with 64% of electricity generation dependent on imported coal and gas, followed by South Korea at 56%, while Italy leads European markets at 47%.

On the other end of the spectrum, US and Brazil demonstrate minimal vulnerability at zero or 1%. Brazil’s generation mix, approaching 80% renewable penetration dominated by hydro, substantially reduces fossil fuel dependency, while US domestic natural gas and coal production insulates the power sector from international price volatility.

On the other end of the spectrum, US and Brazil demonstrate minimal vulnerability at zero or 1%. Brazil’s generation mix, approaching 80% renewable penetration dominated by hydro, substantially reduces fossil fuel dependency, while US domestic natural gas and coal production insulates the power sector from international price volatility.

China and India, despite continued reliance on coal-fired generation, benefit from predominantly domestic coal supply and only 5-6% of power generation is exposed to imported fuel disruptions as week as rapid renewables growth in recent years.

The Cost Impact: From Manageable to Crushing

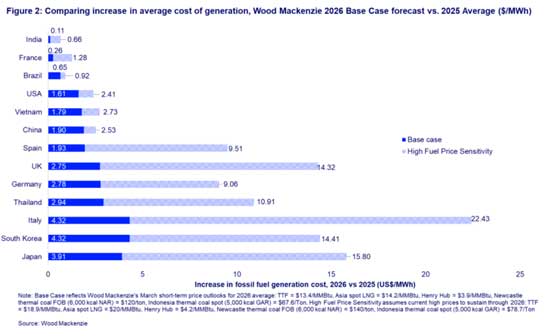

Under Wood Mackenzie’s Base Case, which assumes geopolitical de-escalation enables fuel price moderation in the latter half of 2026, average cost of generation increases by US$2.3/MWh across the 13 analysed markets. Italy, Japan, and South Korea experience the highest absolute impact with US$4.3/MWh in cost escalation.

A High Fuel Price Sensitivity case presents a materially different outlook. Should current elevated price levels persist through 2026, average generation costs would increase 26% on average or about US$8.3/MWh, with the most exposed markets facing substantial cost escalation:

- Italy: US$22.4/MWh (80% increase)

- Japan: US$17.0/MWh (41% increase)

- South Korea: US$14.4/MWh (74% increase)

- UK: US$14.3/MWh (27% increase)

“These cost increases represent significant policy challenges, requiring governments and utilities to navigate difficult trade-offs between financial support mechanisms, regulatory interventions, and retail tariff adjustments,” said Allen Wang, Vice President Head of Asia Pacific Power and Renewables Research for Wood Mackenzie. “For emerging markets with constrained fiscal capacity, elevated fuel costs also translate to heightened reliability risks as securing incremental fuel supplies becomes increasingly challenging during periods of market tightness.”

Beyond financial impacts, fuel supply constraints present direct reliability challenges in markets where import-dependent thermal capacity is central to system adequacy. South Korea faces the most acute exposure, with import-linked thermal capacity equivalent to 87% of peak demand. The government has already implemented electricity conservation policies and emergency fiscal support to reduce peak demand. The crisis is also accelerating a strategic shift, with energy security now rivaling climate policy as a driver of generation investment decisions. Governments are fast-tracking domestic renewable deployment, nuclear capacity additions, and grid infrastructure to reduce import vulnerabilities.

Beyond financial impacts, fuel supply constraints present direct reliability challenges in markets where import-dependent thermal capacity is central to system adequacy. South Korea faces the most acute exposure, with import-linked thermal capacity equivalent to 87% of peak demand. The government has already implemented electricity conservation policies and emergency fiscal support to reduce peak demand. The crisis is also accelerating a strategic shift, with energy security now rivaling climate policy as a driver of generation investment decisions. Governments are fast-tracking domestic renewable deployment, nuclear capacity additions, and grid infrastructure to reduce import vulnerabilities.

These cost increases represent significant policy challenges, requiring governments and utilities to navigate difficult trade-offs between financial support mechanisms, regulatory interventions, and retail tariff adjustments. For emerging markets with constrained fiscal capacity, elevated fuel costs also translate to heightened reliability risks as securing incremental fuel supplies becomes increasingly challenging during periods of market tightness, adds Wood Mackenzie.

It also adds that South Korea faces the most acute exposure: import-linked thermal capacity equivalent to 87% of peak demand provides substantial baseload and mid-merit generation, meaning fuel disruptions directly threaten operational reliability. The government has already implemented electricity conservation policies, demand-side campaigns, and emergency fiscal support to reduce peak demand and limit exposure to higher fuel costs.

Europe’s interconnected market architecture introduces additional complexity, as supply disruptions or price shocks transmit rapidly across borders, potentially converting localised challenges into regional supply concerns.

Emerging markets like Vietnam that have lower ability to pay for high fuel prices may also struggle with reliability should thermal units run low on coal stocks or gas storage and yet can’t compete with richer nations for limited fuel supply in the global market.

Governments are accelerating deployment of domestic renewable generation, nuclear capacity additions, and grid infrastructure while strengthening regional market integration. However, even with this approach, careful policy calibration is being done. European policymakers, for example, face a strategic trade-off: reducing fossil fuel imports requires accepting some technology supply chain dependence (e.g., from China) – while recognising that already installed renewable assets can continue delivering power regardless of supply chain disruptions, whereas fuel dependencies create immediate operational vulnerabilities during geopolitical events.