UAE exits OPEC; to shore up long-term capacity plans

Against the background of years of tension between Abu Dhabi’s capacity expansion ambitions and the constraints of collective quota management, the news on UAE’s decision to exit OPEC+, effective 1 May, has drawn considerable attention from oil market participants.

The move should be understood as a long-term strategic repositioning rather than a reactive response to near-term conditions, according to analysis from Rystad Energy, that views this a deliberate pivot toward capacity-driven competition, with implications that extend well beyond the current period of market volatility exacerbated by tensions in the Strait of Hormuz.

According to Priya Walia, Vice President, Commodity Markets – Oil, Rystad Energy: “The UAE’s exit does not materially alter near-term supply availability, but it reflects a longer-term strategic shift toward greater production flexibility as the country seeks to monetise its expanding capacity base. By stepping outside the quota framework, it reshapes future expectations and weakens OPEC+’s control over spare capacity, as well as the assumption that future supply will be managed through coordinated restraint.”

She added that rather than moving cleanly in one direction, prices are likely to become more volatile, driven increasingly by geopolitical headlines rather than policy signals from OPEC+.

Further out, as the market begins to rebalance, the weakening of OPEC+ as a mechanism to coordinate supply could amplify downside risks compared with previous cycles, she furthered.

The UAE’s exit reflects a long-running tension between its upstream ambitions and the constraints of collective production management.

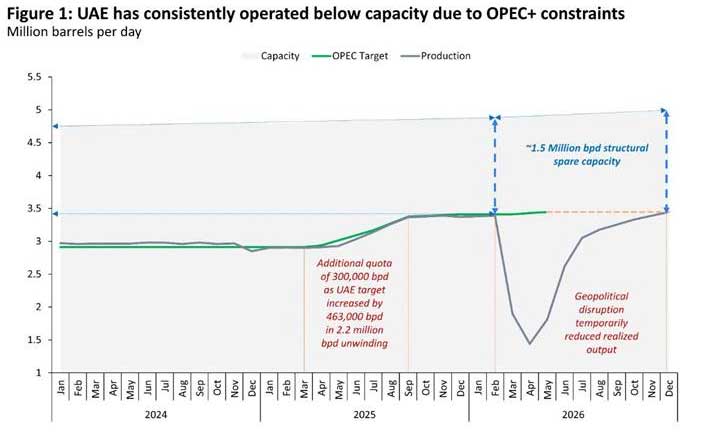

The UAE has consistently operated below its installed capacity for years, with the gap between production and capacity remaining persistent even after OPEC+ granted an additional 300,000 bpd quota allowance as part of the 2.2 million bpd unwind in early 2025.

Prior to the current conflict, the UAE was producing approximately 3.4 million bpd, well below installed capacity, before war-related disruption drove output as low as 1.5 million bpd in April 2026.

ADNOC’s expansion pipeline makes clear why this tension became irreconcilable.

The UAE has a series of brownfield projects either underway or imminent: Upper Zakum Expansion 2 adds 200,000 bpd with a 2026 startup, Bu Hasa contributes a further 90,000 bpd in 2027, and South East Bab brings 130,000 bpd online in 2028, among others.

Source: Rystad Energy research and analysis; Rystad Energy Oil Trading Solution

With a stated target of 5 million bpd of capacity by 2027 and ambitions toward 6 million bpd thereafter, the quota framework was increasingly at odds with the commercial logic of ADNOC’s investment cycle.

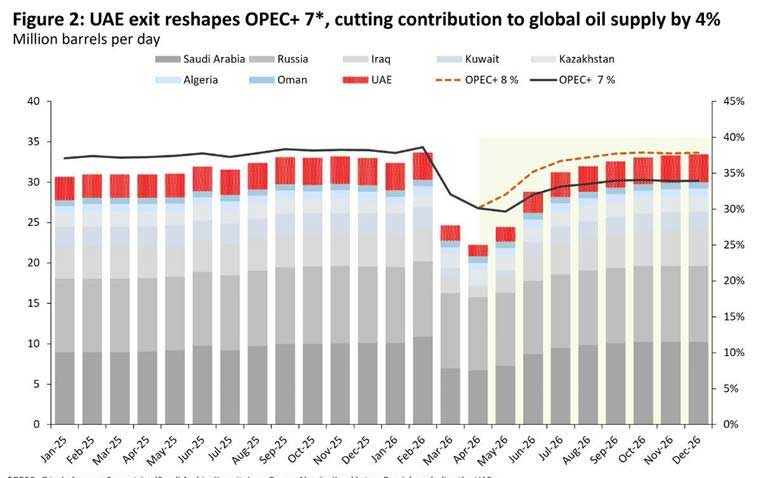

March 2026 OPEC+ compliance data underscores how distorted the production landscape has already become. Total OPEC+ output with quota fell to 27.68 million bpd in March, against a monthly quota of 36.73 million bpd, a shortfall of approximately 9 million bpd driven almost entirely by war-related disruption rather than voluntary restraint.

The UAE itself produced 1.9 million bpd in March against a compensated target of 3.23 million bpd, a deficit of 1.33 million bpd and down 1.49 million bpd from February levels.

*OPEC+ 7 includes core 8 countries (Saudi Arabia; Kuwait; Iraq; Oman; Algeria; Kazakhstan; Russia), excluding the UAE; Crude production from OPEC+ core 7/8 countries as percentage of global crude and condensate supply

Source: Rystad Energy research and analysis; Rystad Energy Oil Trading Solution

Saudi Arabia’s March output of 6.97 million bpd sat 3.14 million bpd below its compensated target, reflecting similar pressures across the Gulf producers most exposed to the conflict.

The pricing environment that emerges from this shift is one defined by competing forces. On one side, geopolitical risk premia remain elevated so long as disruptions around the Strait of Hormuz persist and regional production remains impaired, with UAE realized output expected to only gradually recover toward 3.5 million bpd by end-2026 even under an optimistic scenario. On the other, the prospect of less coordinated supply management, both from the UAE operating independently and from the signal this sends to other producers reassessing their participation, introduces a competing downward force as the market looks ahead to recovery.

Historically, OPEC+ intervention has provided an implicit floor during oversupply episodes, but now that mechanism is structurally weaker.

The transition underway is from policy-driven price stability to capacity-driven competition, a regime shift with lasting implications for price cycle amplitude.

In the near term, prices remain supported by the scale of disruption. In the medium term, as those disruptions unwind, the absence of a robust coordinating framework suggests the recovery phase will be faster and more disorderly on the supply side than previous cycles, with wider price swings and less predictable floors.