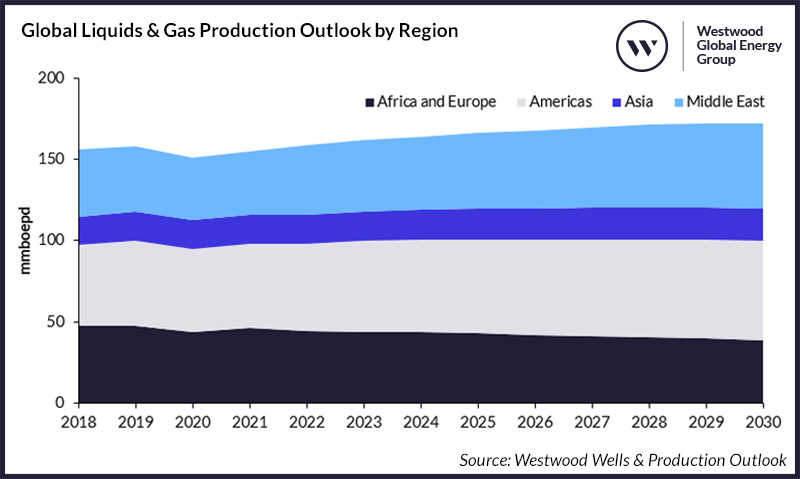

Liquid/gas production expecting 9% growth by 2030

The substantial drilling activity, averaging 53,000 wells per year through to 2030, will help elevate production of crude, condensate, natural gas and natural gas liquids (NGLs) to a high of 173mmboepd by 2030, up 9% from 159mmboepd in 2022, says market research firm Westwood Global Energy in its latest report.

These findings, forming part of Westwood’s Wells & Production Outlook 2023-2030, indicate that 428,000 wells are expected to be drilled over the forecast, with onshore accounting for 95%, dominated by China, Russia and the US. Offshore, more than 17,000 surface wells are forecast, with activities driven by Qatar and Saudi Arabia, while 2,000 subsea wells are expected between 2023-2030, led by the Americas.

Liquids production (crude, condensate and NGLs) is forecast at 100mmbpd by 2030, up 8% on 2022, driven by increased crude production from deepwater areas, such as Brazil and Guyana, as well as additional supply from the Middle East.

Crucially, much of the basis for this supply has been sanctioned. Between Brazil and Guyana 3mmbpd of floating production, storage and offloading (FPSO) capacity have passed final investment decision (FID) but are yet to commence commercial operations, while many of the major expansion projects in Saudi Arabia and the UAE have also been sanctioned, with construction underway.

Gas production is expected to increase 10% by 2030 from new projects in areas such as Mozambique, the Mediterranean, onshore US and brownfield developments, such as the North Field expansion offshore Qatar.

Ben Wilby, Senior Analyst, Westwood said: “The level of investment seen in the last few years will lead to a material increase in structural production capacity over the forecast. As a result, continued OPEC+ intervention will likely be required beyond 2024 to ensure a balanced market and for oil prices to remain at or above Saudi Arabia’s fiscal breakeven range.”

Ben continues: “Deeper oil production cuts in 2Q and 3Q, including an additional 1mmbpd cut by Saudi Arabia, a move intended for July, has been extended to the end of 2023. The cuts could see Saudi Arabian crude production fall to 9mmbpd for much of 2H 2023 with uncertainty over when production will be restored.”

He adds that supply additions, especially in the latter years of the forecast, remain at the pre-sanctioning stage, which represents a downward risk to expected output, especially if prices drop below US$60/bbl.