2022: US in running as largest LNG exporter; China top LNG importer

The world’s two largest economies, US and China, are poised to be the world’s top export and import markets for liquefied natural gas (LNG) in 2022, says a new report by research firm IHS Markit.

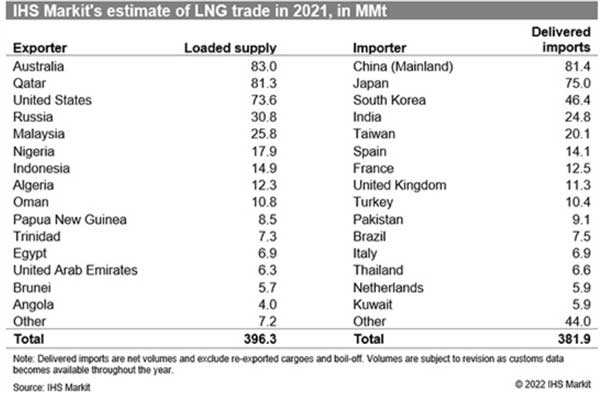

The report, entitled LNG Trade in 2021: Runaway Recovery finds that the US, which was the third-largest LNG exporter behind Australia and Qatar for the full year of 2021, is poised to claim the top spot in 2022. The US was the largest source of LNG supply growth in 2021, adding 25 million metric tons (MMt) amid continued buildup of liquefaction capacity as well as the ramping up of output from plants turned down the previous year. Average utilisation for US plants climbed from 43% in third quarter 2020 to 98% in third quarter 2021.

Meanwhile, China has already become the top global importer of LNG. Imports reached 81 MMt in 2021 (increase of 12.3 MMt or 18%), overtaking Japan where imports were flat year-over-year at 75 MMt. This marks the first time since the early 1970s that Japan has not been the world’s largest LNG importer.

“A new map of LNG is taking shape as 2021 became the year of rapid recovery, making the oversupply and price lows of 2020 seem like a distant memory,” said Michael Stoppard, chief strategist, global gas, IHS Markit. “It is a tale of two markets with China fueling the demand surge as the world’s top importer and the United States, poised to become the world’s leading exporter, providing the supply push.”

Among other key LNG trends observed in the report:

- Long-term contract signings rebounded to an all-time high after a pause in 2020. Over 65 million metric tons per annum (MMtpa) of firm, long-term contracts were signed in 2021, surpassing the previous record of 61 MMtpa in 2013. Among sellers, signings were roughly evenly split between the US, Russia, Qatar and portfolio suppliers (although many of the latter are likely to source volumes from US projects). In a notable signpost of potential investment trends in 2022, US projects were by far the largest source of pre-final investment decision (FID) contracts, as most contracts signed in Qatar and Russia were for capacity that is either already existing or under construction. Among buyers, mainland China was by far the largest specified end-market, with Chinese buyers signing around 25 MMtpa of firm long-term deals.

- Spot LNG prices have soared past previous records. Spot LNG prices in Asia spiked to nearly US$30 per million British thermal units (MMBtu) for a few weeks in January 2021 during extreme cold weather and transportation challenges before settling back to normal ranges in the first half of the year. However, by August both Asian and European spot LNG prices climbed well above their oil price equivalent and remained above it for the rest of the year. Prices ended December 2021 at US$40/MMBtu—more than double the previous peaks achieved in the several years following Japan’s 2011 nuclear crisis.

- Brazilian imports hit all-time high amidst drought. Persistent dry weather in Brazil resulted in weak hydropower generation, forcing the market to rely more heavily on LNG imports. Brazil more than tripled its 2020 imports by receiving 7.5 MMt in 2021, surpassing the previous record of 5.8 MMt set in 2014.

- Amid strong global demand, European LNG imports fell. As one of the most flexible regional import markets in the world, European LNG deliveries are reflective of global market balances. Given strong demand in Asia and South America, less LNG supply was available to Europe and European LNG deliveries fell by 9% (7 MMt) in 2021 to 77.2 MMt. However, this is well above the region’s average import level (30-40 MMt) during previous years of LNG market tightness (2012-2018) as imports were kept relatively high by cold weather and low storage levels.

- Outside of the US, utiliSation rates suffered. Throughout the year, plants across the Atlantic and Pacific Basins faced unexpected outages and gas feedstock shortfalls from maturing production, dragging down average global utilization below the previous five-year average (excluding the price-responsive shut-ins in the US in 2020). Utilisation was particularly weak during the summer in the northern hemisphere, with non-US global utilisation averaging 11 percentage points lower than the five-year average.

For more information about the report LNG Trade in 2021: Runaway Recovery or about IHS Markit LNG research services visit https://ihsmarkit.com/products/LNG-market-outlook-demand-forecast.html