BloombergNEF drops key findings in 1H 2021 Battery Metals Outlook report

According to BloombergNEF (BNEF), a strategic research provider covering global commodity markets and the disruptive technologies driving the transition to a low-carbon economy, battery metal prices have recovered strongly in the first half of the year, incentivising new projects to come online. China maintained its grip on the battery chemical industry, with the biggest market share for all the five main battery metals. Indeed, diversifying the global supply chain would require significant investment from regions such as Europe and North America.

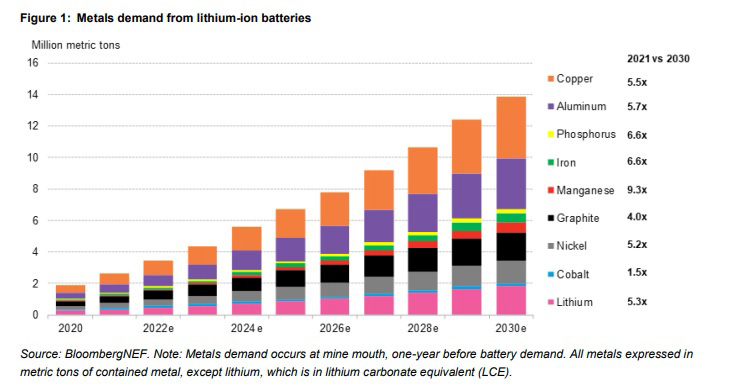

BNEF’s latest Battery Metals Outlook says that diversifying the global supply chain would require significant investment from regions such as Europe and North America. By 2030, under our economic transition scenario, annual demand for lithium-ion batteries will pass 2.7TWh per year. Total annual battery demand in 2030 is 35% higher than in last year’s outlook, largely due to higher demand from passenger EVs.

Rise in metal prices could impact chemistry adoption but not EV uptake

Sustained high raw material prices could result in a significant shift in battery chemistry mix. Automakers could switch to lithium iron phosphate (LFP) chemistry, which would reduce the performance of some EVs, particularly their range. But this would enable the electrification of transport to continue unabated. In our LFP scenario, we increase LFP’s share of stationary storage deployments in 2030 from 23% to 53%, at the cost of the highest nickel chemistries.

Lithium well supplied up to 2025

The carbonate and hydroxide should be sufficiently supplied until at least 2025. Hydroxide could face a shortage by 2027, as demand for high-nickel chemistries surges. One key risk is that about 35% of the projected supply growth from now until 2025 will come from integrated spodumene-to-hydroxide converters in Australia. These projects are expensive and have had a history of delayed development. Should these Australian converters delay in their commissioning hydroxide could be in shortage by 2025.

Lithium prices to rise further but plateau by 2022

Lithium prices continued to rise in 2021 due to the restraint in supply as a result of the pandemic and the higher demand recorded in China and Europe. Lithium prices have climbed 71% for carbonate this year, 91% for hydroxide and 58% for spodumene concentrate. We expect all prices to continue their rally but gradually plateau as more supply come online in 2021-2022.

Nickel sulfate balance to slip into deficit

The nickel sulfate market remains in balance in the near term, despite the increased demand expected in the next five years. Domestic demand in China was relatively low as some automakers shift to LFP chemistries. This will have limited impact in the adoption of nickel-rich battery cathode chemistries, and as such, the nickel sulfate market balance may slip into a 128,000 tonne deficit as early as 2024.

Nickel prices to hold steady

At the start of the year, BNEF predicted that the nickel market will move into a two-tier system for nickel pricing to further incentivize investment into additional Class 1, battery-grade nickel supply. At the end of the first half of 2021, there have been no concrete developments toward this much needed change in the dynamics of pricing in the nickel market. Prices will likely remain within US$18,000/tonne for 2021.

Cobalt surplus looms

The cobalt market is likely to be in a narrow surplus this year. Both large-scale and artisanal miners will produce about 166,434 tonnes of cobalt in 2021. Demand for cobalt will reach 163,121 tonnes in 2021, leading to a 3,313-tonne surplus this year. This projected surplus will be dependent on the ability of artisanal producers to ramp up supply.

Cobalt price to hold

Cobalt metal prices have risen by 42% year-to-date on the London Metals Exchange. In March, it rose to US$53,000/tonnes. This is the highest price since March 2018 and 15% above the five-year average. The cobalt metal price could average US$45,000/tonne year-end 2021. With the market projected to be relatively in surplus this decade, we expect prices will hold at an average of US$44,000/tonne up to 2025.

Manganese supply recovers strongly

Manganese production in South Africa increased in April by 208% year on year. The market has recovered strongly from the impact of Covid-19. In spite of the resumption of mine operations in South Africa, the industry has been saddled with challenges associated with haulage, electricity reliability and port operations.

Manganese sulfate prices to rise

Manganese sulfate prices have risen by 30%, from US$867/tonne in January to US$1,128 in June, due to an increase in battery demand. Prices are likely to keep rising in the second half of the year as demand for batteries is projected to grow. With the manganese sulfate market currently projected to be in a deficit, prices are likely to rise to support new refinery projects in order for supply to meet demand by 2024.

Graphite demand to grow

Graphite demand from lithium-ion batteries is set to rise year-on-year by 37% to 446,914 tonnes in 2021, BNEF estimates. It will grow by 297% by the end of the decade. Commercial vehicles will represent the fastest growth, with year-on-year demand doubling in 2021. Overall, graphite demand from lithium-ion batteries will reach 446,914 tonnes in 2021.